Weekly Insights for Dubai Property Investors: November 15, 2025

- Stephen James Mitchell MBA

- Nov 15, 2025

- 5 min read

Updated: May 19

As we close the week ending November 15, the UAE’s macroeconomic picture continues to highlight a consistent theme: steady strength underpinned by diversification. Dubai recorded 4.4% GDP growth in the first half of the year, led by construction, real estate, and financial services. Abu Dhabi, meanwhile, is on track for 6% growth in 2025, supported by a recovery in oil output and rising manufacturing activity.

Taken together, these figures offer further reassurance for investors watching the region closely. Many global economies are still grappling with inflation, shifting trade dynamics, and geopolitical risk. Despite this, the UAE has maintained steady forward momentum. The property sector continues to play a particularly central role in that resilience.

This week’s summary breaks down where that momentum is coming from. We’ll look at what’s changing across both residential and commercial sectors. We’ll also explore how investor behaviour is adapting, shaped by a growing pipeline of new projects and a shifting interest rate environment.

If you’d like to see which projects stand to benefit most from these shifts, get in touch now. I’ll share a focused shortlist of opportunities aligned with the current market direction.

Economic Performance: Broad, Not Overheated

Dubai’s economy grew 4.4% in H1 2025, reaching AED 241 billion. What stands out to me is the diversity of contributors: construction up 8.5%, real estate up 7%, and financial services up 6.7%. These numbers point toward a balanced expansion rather than one driven by a single outperforming sector.

In Abu Dhabi, the IMF’s revised 6% GDP expectation reflects a combination of higher oil output and sustained non-oil activity — notably in manufacturing and tourism. The ability of both emirates to maintain parallel growth paths suggests a degree of resilience in the wider UAE economy.

For property investors, this type of growth profile matters. It reduces dependency on single-sector cycles and tends to support more predictable real-estate demand.

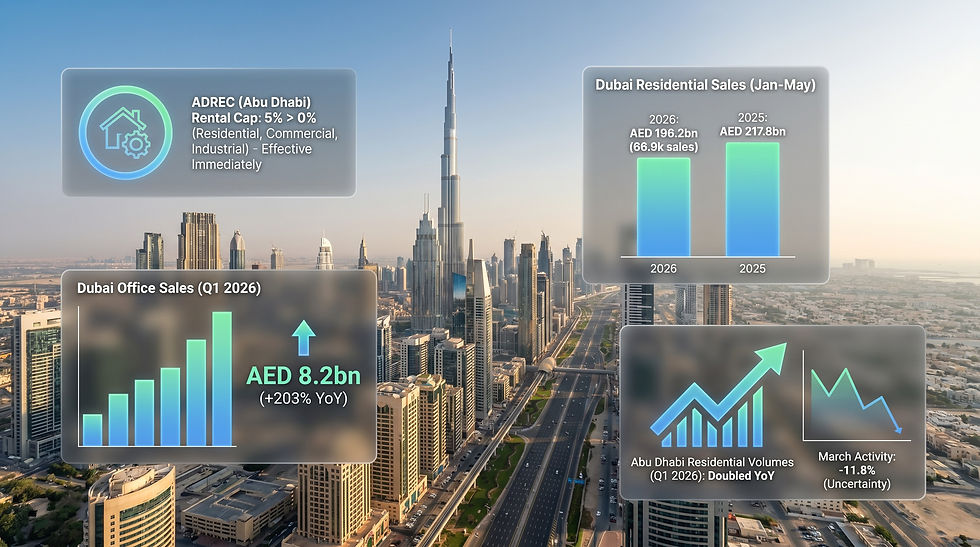

Property Market Activity: High Volumes With Signs of Normalisation

Dubai recorded more than 177,000 property transactions year-to-date, an 18% increase over the same period in 2024. October contributed over AED 46 billion in sales, continuing the pattern of high deal activity seen throughout the year.

The composition remains broadly consistent:

Residential makes up roughly 87% of all transactions

The primary market accounts for around 70% of sales

A high primary-market share is not unusual in Dubai during phases of new-supply expansion. Developers are releasing units at a steady pace, and payment plans remain a key driver of accessibility, particularly for end-users transitioning from rental.

Key communities — Jumeirah Village Circle, Dubai Hills Estate, and Business Bay — continue to see strong activity due to their mix of price points, amenities, and connectivity. Price growth of approximately 16% year-on-year indicates demand remains firm, though the rate of appreciation appears more controlled than earlier in the cycle.

Supply and Developer Positioning: A More Strategic Landscape

The moderation in price acceleration is consistent with a market where new supply is gradually increasing. Developers remain active, but the approach is more segmented.

Mid-market and family-oriented communities continue to receive attention, while flagship luxury launches proceed at the upper end. A notable example is Emaar Hills, where Emaar Properties recently introduced Dubai Mansions, a AED 100 billion master development consisting of approximately 40,000 high-end homes, including palatial residences.

The scale of this project indicates confidence in long-term demand for luxury housing, but it also highlights the widening differentiation between market tiers.

For investors, this means the supply picture is becoming more varied, which may require a more detailed assessment of micro-locations and specific asset types.

Commercial Property: Consistent Outperformance

One of the most notable trends this year — and again this week — is the continued strength of the commercial sector.

Dubai’s commercial sales reached AED 30.38 billion in Q3 2025, up 31% year-on-year. Areas such as Business Bay and Jumeirah Lake Towers remain central to this momentum.

Several indicators stand out:

Prime office vacancy is now below 8%

Average rents have risen 17% year-on-year

Demand continues to come from tech, fintech, and logistics sectors

New supply remains structurally constrained in free zones

These fundamentals suggest the office market is still tightening rather than loosening. For investors, this segment remains one of the few where yields have not compressed significantly despite broader economic shifts.

The growth of flexible office operators also indicates that smaller and mid-sized companies are committing to local bases rather than relying on remote or offshore operations — another subtle yet important signal of deepening business activity.

Explore commercial listings and insights at Mitchell’s Commercial Realty — featuring premium office and retail properties across Dubai, along with market intelligence to help you identify emerging trends.

Tourism, Population, and Demand Stability

Tourism remains another consistent pillar. Dubai recorded 12.5 million international visitors so far this year — a 6% increase — keeping the city on track for one of its strongest tourism performances to date.

Hotel occupancy remains around 81%, while the hospitality development pipeline continues to expand, with over 1,100 hotel projects in planning or construction.

Population trends are equally relevant. Dubai’s population has now surpassed 4 million, supported by employment creation, long-term residency schemes, and ongoing migration from higher-tax jurisdictions. This provides a stable foundation for both rental and owner-occupier demand.

Fiscal Policy and Rates: A Predictable Backdrop

The federal government approved a AED 92.4 billion budget for 2026, continuing its emphasis on healthcare, education, and infrastructure. The sustainability of federal spending, supported by solid reserves and diversified revenue sources, provides long-term clarity for investors and developers.

Meanwhile, the second rate cut of 2025 has begun to filter into borrowing costs. Early signs show increased mortgage uptake, particularly in communities where prices have stabilised. This may become a more visible theme over the next two quarters as affordability gradually improves.

S&P Global’s reaffirmation of the UAE’s “stable” outlook — citing fiscal buffers and diversified growth — reinforces the general sense of policy continuity.

Key Takeaway: A Market Defined by Balance, Not Excess

Across all the data points this week, one theme is consistent: balance.

Growth is continuing, but at a measured pace. Prices are rising, but not accelerating unsustainably. Supply is increasing, but developers are segmenting rather than flooding the market. Tourism is expanding, and population growth remains steady.

For investors, this environment rewards selectivity. The broad market is healthy, but performance is no longer uniform. Opportunities now depend more on asset type, location, entry structure, and timing.

Commercial assets, well-priced residential resales, and properties in communities with strict supply constraints continue to show the strongest fundamental support. Meanwhile, relying solely on headline trends may overlook nuances that matter at this stage of the cycle.

Conclusion

As we move through November, Dubai’s property market continues to demonstrate a combination of stability and depth — supported by solid economic performance, consistent population growth, and a clear policy environment. While new supply and rate changes may influence short-term behaviour, the broader fundamentals remain positive.

The key now lies in selectivity. Investors who position early in resilient communities, high-yield commercial assets, or hybrid-use opportunities stand to benefit most as the market continues to evolve.

If you’d like to explore a tailored shortlist of opportunities backed by current market data and my 18+ years of on-the-ground insight, I’d be glad to assist.

📞 No pressure, no sales pitch—just a focused, informed conversation about your investment goals. Let’s talk.