Weekly Insights for Dubai Property Investors: June 13, 2026

- Stephen James Mitchell MBA

- Jun 15

- 7 min read

This was a week of deliberate contrasts. Emaar unveiled an AED 200 billion (USD 55 billion) master-planned district for 150,000 residents, and AHS Properties paid AED 1.1 billion for the Shangri-La hotel on Sheikh Zayed Road — two of the largest commitments by developers we have seen since the conflict began.

Yet the official data told a more measured story. Capital values fell for a third consecutive month in May, ready-home transactions dropped sharply year-on-year, Dubai International passenger traffic was down around 20% in Q1, and the World Bank cut its global growth forecast to 2.5% — the weakest since the pandemic.

The Iran conflict remains the variable sitting behind all of it. For investors, what stands out is resilience alongside a rising risk premium — liquidity and top-end demand are holding, but pricing is cooling, and the cost of being wrong has gone up.

If you're reassessing your positioning in this market, I can show you where risk-adjusted opportunities are emerging. Click here to speak with me directly.

Emaar Commits to an AED 200 Billion District — the Decade's Biggest Vote of Confidence

Emaar announced plans to develop an AED 200 billion (USD 55 billion) master-planned district designed for nearly 150,000 residents. The 4.5 million square metre development spans towers, villas, mansions, offices, retail, and hospitality across five character zones, built around a "20-minute city" concept.

A capital commitment of this scale, announced by the emirate's largest developer in the middle of a regional conflict, is the clearest possible statement about how the market's biggest player views Dubai's decade ahead. It is not a cyclical bet; it is multi-year infrastructure underwriting that assumes sustained population and demand growth well into the 2030s.

For investors, a commitment at this scale supports long-term land and community values along the growth corridors. But it also adds materially to the future supply pipeline. Supply, not demand, is the variable most likely to cap rental growth and secondary-market pricing as this one and similar megaprojects deliver.

The announcement is a reason for optimism on direction, and a reason for discipline on entry price and exit timing.

AHS Buys the Shangri-La for AED 1.1 Billion as Prime Sheikh Zayed Road Values Climb

AHS Properties acquired the Shangri-La hotel on Sheikh Zayed Road for AED 1.1 billion (USD 272 million) from Abu Dhabi's Mismak, a First Abu Dhabi Bank unit, in the largest single-asset transaction of the week. The 42-floor, roughly 93,000 square-metre tower is the developer's second major Sheikh Zayed Road purchase, and the firm plans to launch a separate AED 25 billion mixed-use project on the Dubai Water Canal later this year, taking its development portfolio toward AED 50 billion.

Prime central land and hospitality assets transacting at this level — while the broader market softens — tells you capital is concentrating into scarce, trophy-grade positions rather than retreating wholesale.

That said, balance matters. Perceived risk on UAE property has risen since the conflict began, even as the top of the market continues closing landmark deals. Both things are true at once — confidence at the highest end, and a higher risk premium underneath it. Sophisticated investors should hold both facts in view.

The Cooling Is Real, but It Is Decelerating

ValuStrat Price Index — May 2026 | Data |

Capital values, month-on-month | -1.2% (Mar -5.9%, Apr -1.9%) |

Capital values, annual | +2.5% (still positive) |

Villas, month-on-month | -1.4% (+5% year-to-date) |

Apartments, month-on-month | -0.9% (-1.4% year-on-year) |

Ready-home transactions | -18.5% MoM, -55% year-on-year |

Underneath the headline deals, the most important market-direction data came from the ValuStrat Price Index, showing Dubai capital values fell 1.2% in May — a third consecutive monthly decline, but a markedly slower one than the 5.9% drop recorded in March.

The shape of that decline matters more than the direction. Three straight monthly falls confirm the cycle has turned from its 2024–25 peak. But the deceleration — from nearly 6% in March to barely over 1% in May — and the still-positive 2.5% annual figure suggest a market finding a floor rather than entering a rout.

The sharp drop in ready-home transactions is the clearer signal of buyer caution: completed-property buyers, who tend to be end-users and yield investors, have pulled back hardest, while off-plan continues to attract committed capital.

Liquidity Holds: AED 28.5 Billion in May, AED 11.3 Billion in the Latest Week

Dubai DLD — May 2026 | Value | Deals |

Total activity | AED 28.51 billion | 10,218 |

Residential | AED 22.01 billion | 9,507 |

Commercial | AED 6.50 billion | 711 |

Transaction liquidity, by contrast, remains substantial. Dubai Land Department data shows AED 28.51 billion across 10,218 transactions in May, and the most recent weekly figures recorded a further AED 11.3 billion across 4,086 transactions.

The composition is the point. Prices are softening at the same time volumes remain healthy — which is what an orderly repricing looks like, not a liquidity crisis.

Within the latest week's AED 11.3 billion, sales accounted for roughly AED 7.4 billion across 3,111 deals, with mortgages and gift transfers making up the balance. Buyers are still transacting in size; they are simply negotiating harder on price.

Explore curated office and retail opportunities at Mitchell's Commercial Realty.

The Top End Keeps Absorbing Capital: AED 4.96 Billion in Luxury Off-Plan

The divergence between the cooling mid-market and the resilient top end was visible again in May, when luxury off-plan homes priced above AED 5 million recorded AED 4.96 billion in sales across 391 transactions, at an average of AED 12.7 million per property. Villas (AED 2.51 billion) edged apartments (AED 2.45 billion).

This is the same pattern that has defined the market through the conflict. At the ultra-prime end, where buyers are typically cash-rich and acquiring scarce, branded or waterfront product, demand has barely flinched. These buyers treat periods of volatility as acquisition windows.

The cooling captured by the ValuStrat index is overwhelmingly a mid-market and secondary-market phenomenon; the luxury new-build segment is operating on a different cycle.

Government Keeps Broadening Demand: First-Time Buyers and Earlier Financing

Two policy-led developments this week were aimed squarely at widening the buyer base. Dubai's first-time homebuyer programme has now generated more than AED 5 billion (USD 1.36 billion) in sales and over 3,200 first-time owners since July 2025. Around 45,000 residents have registered, supported by five banks. This week, nine more developers joined the programme, bringing the total to 22.

Separately, Dubai Holding Real Estate and Commercial Bank of Dubai launched an early home-financing programme for buyers across the Nakheel, Meraas, and Dubai Properties portfolios, giving eligible purchasers structured access to financing earlier in the buying journey.

Both measures matter to investors because they are structural, not cyclical. They deepen the end-user base beneath the speculative layer of the market — exactly the kind of demand that stabilises pricing and rental absorption through a softer patch.

Sharjah's Record Run Confirms the Northern Emirates Story

Capital is also diversifying beyond Dubai and Abu Dhabi. Sharjah's property sales reached an all-time high of AED 65.6 billion in 2025. Q1 2026 transaction values rose 41% to AED 18.5 billion across roughly 9,980 deals — a 23% increase in volume. The emirate has around 33,700 units in its delivery pipeline to 2030, split between roughly 24,800 apartments and 9,900 villas and townhouses.

As Dubai yields compress and Abu Dhabi rents sit under a freeze, the relative value on offer in Sharjah is drawing yield-seeking capital northward.

For investors comfortable with the additional liquidity and exit considerations of a thinner market, the Northern Emirates remain one of the clearer relative-value plays in the country right now.

The Macro Backdrop: A Global Downgrade, a Sovereign Affirmation, and a War Discount

Three macro developments framed every UAE property decision this week.

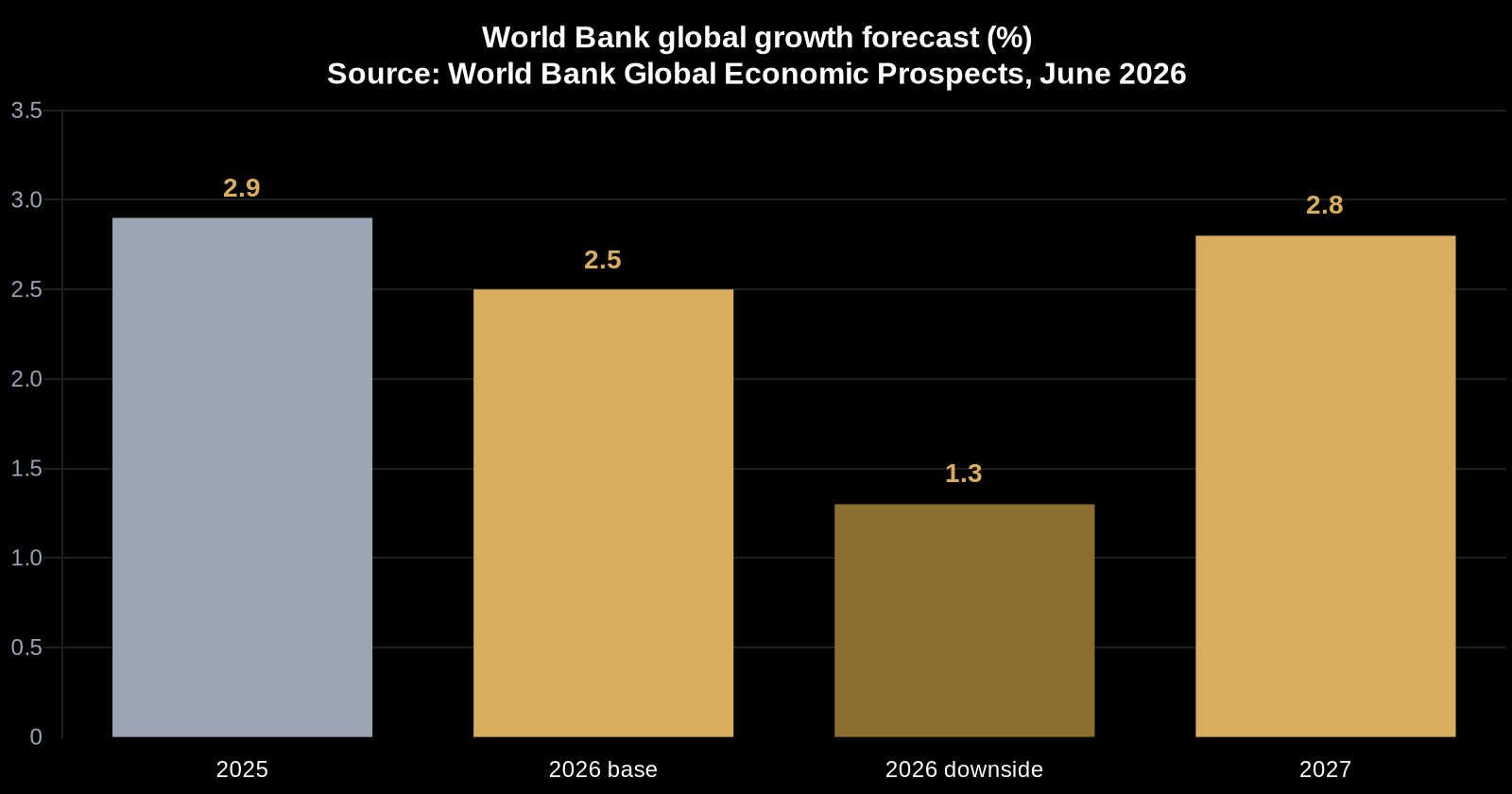

First, the World Bank cut its 2026 global growth forecast to 2.5% — the weakest pace since the pandemic, down from 2.9% in 2025. If the conflict persists and the Strait of Hormuz stays closed, with oil near USD 115, the World Bank says growth could fall as low as 1.3%. A recovery to 2.8% is projected for 2027.

Second, the war is leaving a visible mark on Dubai's real economy. Dubai International handled 18.6 million passengers in Q1, down around 20% year-on-year. March traffic fell sharply following the late-February disruption — a hard demand indicator that feeds directly into hospitality, short-stay and retail-linked assets.

Third, the country's financial buffers held firm despite that pressure. Moody's affirmed the UAE's Aa2 rating with a stable outlook, citing strong shock-absorption capacity, with Abu Dhabi's foreign assets estimated at around 300% of GDP.

UAE Outlook | Reading |

Moody's rating | Aa2, stable outlook |

Abu Dhabi sovereign assets | ~300% of GDP |

World Bank UAE growth | 2.4% (2026) → 4.1% (2027) → 4.2% (2028) |

2025 UAE real GDP | AED 1.9 trillion (USD 517 billion), +6.2% |

Moody's projects a steep near-term GDP contraction for 2026 before recovery. The IIF described the UAE's slowdown as temporary, expecting the country to recover fastest from the conflict, with the World Bank forecasting UAE growth of 2.4% in 2026, followed by a rebound above 4% in 2027–28.

The picture remains consistent: substantial balance-sheet strength is absorbing a real, war-driven demand shock. The fundamentals support a recovery — how quickly it arrives now depends on how the conflict progresses.

Dubai's Top Communities Are Up to 153% Above 2021 Levels Despite Recent Softening

The current softening should be read against the scale of the run-up that preceded it. Data from Bayut shows advertised prices in Dubai's strongest communities are up between 41% and 153% from May 2021 to April 2026. Jumeirah Islands leads at +153%, followed by Jumeirah Golf Estates (+119%), Jumeirah Lake Towers (+115%), Dubai Hills Estate (+87%) and Palm Jumeirah (+83%). These are advertised, not transacted, prices — but the scale of appreciation puts the recent softening in context.

A market that has nearly doubled in value over five years and is now retreating by low single digits per month is undergoing a correction, not a collapse. For long-horizon investors, that distinction matters more than the headline monthly figures.

Final View

Taken together, the evidence points to a market in the early stages of a transition rather than a downturn. For the past two years, the story has been about how much demand the market could absorb. The current data suggests the question is now shifting — toward how much of a slowdown the market's underlying strength can absorb before pricing stabilises again.

Capital commitments at the scale seen this week only make sense if the people deploying them expect that floor to hold. The next several months will show whether the deceleration in price declines continues, or whether it stalls — and that will say more about the next 12 months than any single transaction can.

Let’s Talk

If you’d like to unpack where the most resilient opportunities are emerging — in stabilised residential areas or income-generating commercial zones — I’d be happy to share a focused, data-driven shortlist based on your investment goals.

📞 No pressure, no sales pitch—just a focused, informed conversation about your investment goals.